Most buyers obsess over “What’s the lowest price I can get?” when they should be asking, “What’s the lowest monthly payment I can get for this home?” In today’s interest‑rate environment, focusing on monthly payment—and using seller credits strategically—can save you far more than a small price cut.

Buyer Pro Tip: It’s Not Just the Price, It’s the Payment

When you’re buying a home, your lifestyle is built around the monthly payment, not the sticker price on the listing. Your payment is driven by three main factors: price, interest rate, and loan terms.

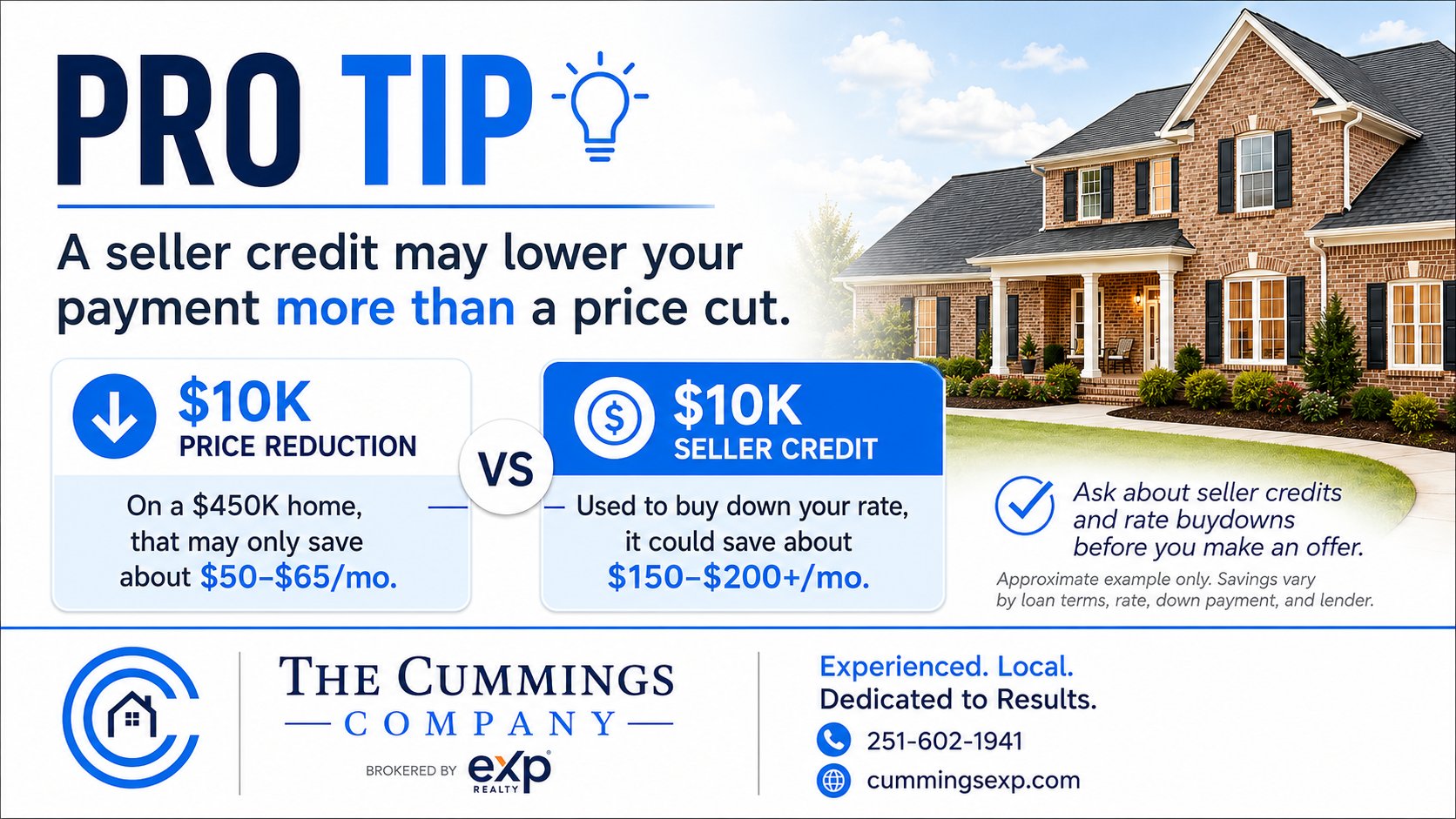

On a 450,000 dollar home, a 10,000 dollar reduction in price might feel like a big win. But once that discount is spread out over a 30‑year mortgage, the impact on your monthly payment can be surprisingly small—often in the ballpark of only 50–65 dollars per month, depending on your rate and loan program.

Now compare that to using the same 10,000 dollars as a seller credit to buy down your interest rate. When you apply that money toward discount points and closing costs, it can lower your rate enough to shave roughly 150–200 or more off your monthly payment, again depending on your loan structure and current rates. Same 10,000 dollars, very different monthly outcome.

Price Reduction vs. Seller Credit: What’s the Difference?

Let’s break down the two options you might negotiate into your offer:

-

Price reduction

-

Lowers the purchase price and loan amount slightly.

-

Usually creates only a modest drop in monthly payment.

-

Helps a bit with long‑term equity and can matter for appraisal.

-

-

Seller credit

-

The seller contributes money toward your closing costs or interest rate buydown.

-

Can be used to buy discount points and reduce your rate.

-

Often produces a much larger monthly payment reduction than the same dollar amount off the price.

-

For most financed buyers, especially those planning to stay in the home for several years, the seller credit focused on a rate buydown often delivers more real‑world savings than a small price cut.

A Simple Example on a $450,000 Home

Here’s a simplified way to think about it:

-

Option 1: 10,000 price reduction

-

Purchase price drops from 450,000 to 440,000.

-

Your loan amount goes down slightly.

-

The monthly payment bump is noticeable—but usually modest—because the interest rate stays the same and the change is spread over many years.

-

-

Option 2: 10,000 seller credit for a rate buydown

-

Purchase price stays at 450,000, but you receive 10,000 as a credit at closing.

-

That credit is used to pay discount points and reduce your interest rate.

-

A lower rate reduces the cost of every dollar you borrow, which can slash your monthly payment by 150–200 or more.

-

While exact numbers will vary based on your credit, down payment, loan type, and current rates, the concept is the same: using negotiation power on the interest rate instead of just the price can give you a much stronger monthly win.

Why Monthly Payment Should Drive Your Strategy

Your monthly payment affects everything:

-

Your comfort level with the home you choose.

-

Your ability to save, invest, or handle emergencies.

-

Your approval and debt‑to‑income ratio with the lender.

When you negotiate, think in terms of “payment strategy” rather than “price-only strategy.” Instead of saying, “I want 10,000 off the price,” ask, “What structure gets me the best monthly payment: price reduction, seller credit, or a mix of both?”

Working with a local lender, you can compare side‑by‑side scenarios before you write the offer. That way you’re not guessing—you’re choosing the path that gives you the strongest monthly advantage.

How to Talk to Your Lender About This

Before you submit an offer, ask your lender to run at least two scenarios:

-

450,000 purchase price with a 10,000 price reduction.

-

450,000 purchase price with a 10,000 seller credit applied to closing costs and a rate buydown.

Have them show you:

-

The monthly principal and interest payment in each scenario.

-

How much interest you’ll pay over the first 5–7 years.

-

Your break‑even point—how long you need to stay in the home for the buydown to make sense.

With this information, you and your agent can decide which structure to ask the seller for and how to position your offer to win the home while protecting your budget.

Local Impact: Mobile & Baldwin County Buyers

If you’re shopping in Mobile or Baldwin County, the stakes are real. Prices, taxes, insurance, and HOA fees can vary from neighborhood to neighborhood, and every piece affects that final monthly number.

In a competitive coastal market, using a smart seller‑credit strategy can help you:

-

Afford the neighborhood you really want instead of settling.

-

Stay within a comfortable monthly payment even if rates fluctuate.

-

Make stronger, cleaner offers that still fit your long‑term budget.

This is where local expertise matters. A local agent and lender team can look at real numbers for homes in West Mobile, Midtown, Eastern Shore, or Baldwin County beach communities and help you structure an offer that fits your life—not just the list price.

Ready to Run Your Numbers?

Before you make an offer, make sure you understand all your options—because the right strategy could save you more money every single month.

If you’re thinking about buying in Mobile or Baldwin County, let’s talk through your goals, your budget, and your best negotiation strategy before you write your next offer.

The Cummings Company

Experienced. Local. Dedicated to Results.

📞 251‑602‑1941

🌐 cummingsexp.com